Hyperinflation Hyperbole

Janet Yellen invokes hyperinflation. A financial historian pushes back.

In 2021 and 2022, the hyperinflation bros emerged from the woodwork. Amateur hour on finTwit.

We were in the midst of the highest inflation in forty years, but none of the hyperinflationary kind. Prices rose a bit, not a thousandfold. The bros retreated.

Now there’s a new Baba Yaga story, retold by a credentialed expert. But is the bogeyman real this time?

Is hyperinflation back on the menu?

Janet Yellen, former Fed Chair and Treasury Secretary, is a qualified expert in all things monetary, so people listen when she says things like:

How often does the president of a developed country express the view that interest rates should be set to reduce the debt service costs of the federal debt? … That is the story of high and even hyperinflation in every country that has suffered it. And that is what President Trump is saying.

And, a week later, in Fortune:

“That’s the road in a banana republic to high or even hyperinflation.”

Yellen knows what hyperinflation means. Unlike, say Michael Burry,Jack Dorset or Michael Saylor. Which makes her choice of word interesting. Not imprecise by accident, almost certainly.

But “hyperinflation” is doing a lot of heavy lifting in her speeches, and it deserves to be examined.

I’m a financial historian, not a monetary economist. An ex-distressed credit hedgie, not a macro trader. But I’ve spent enough time in the archive to know that hyperinflation has a specific definition, a specific cause, and a specific history. And the “rate cuts → hyperinflation” narrative doesn’t fit any of them.

The real concern here is credibility, not Cagan-like price increases of 50% per month (the standard for hyperinflation accepted by most economists). Will Kevin Warsh come in as Fed Chair and cut rates solely because his boss in the White House says so?

That’s a legitimate concern. The credibility that was hard-won by Volcker and mostly frittered away ever since, matters for inflation expectations. Warsh surrendering it to political pressure would be damaging.

But “damaging” is not “Weimar.” Hyperinflation, of Weimar Germany proportions, is extremely unlikely to be caused by a Warsh-Trump coalition to cut rates. At least not directly and if it’s limited to just that.

Let me explain why.

There is no rate cut Baba Yaga

Hyperinflation is not just “inflation that feels very bad”. It means prices have to double every six weeks or so.

Hyperinflation in history has never been caused by a few 100 bps rate decline.

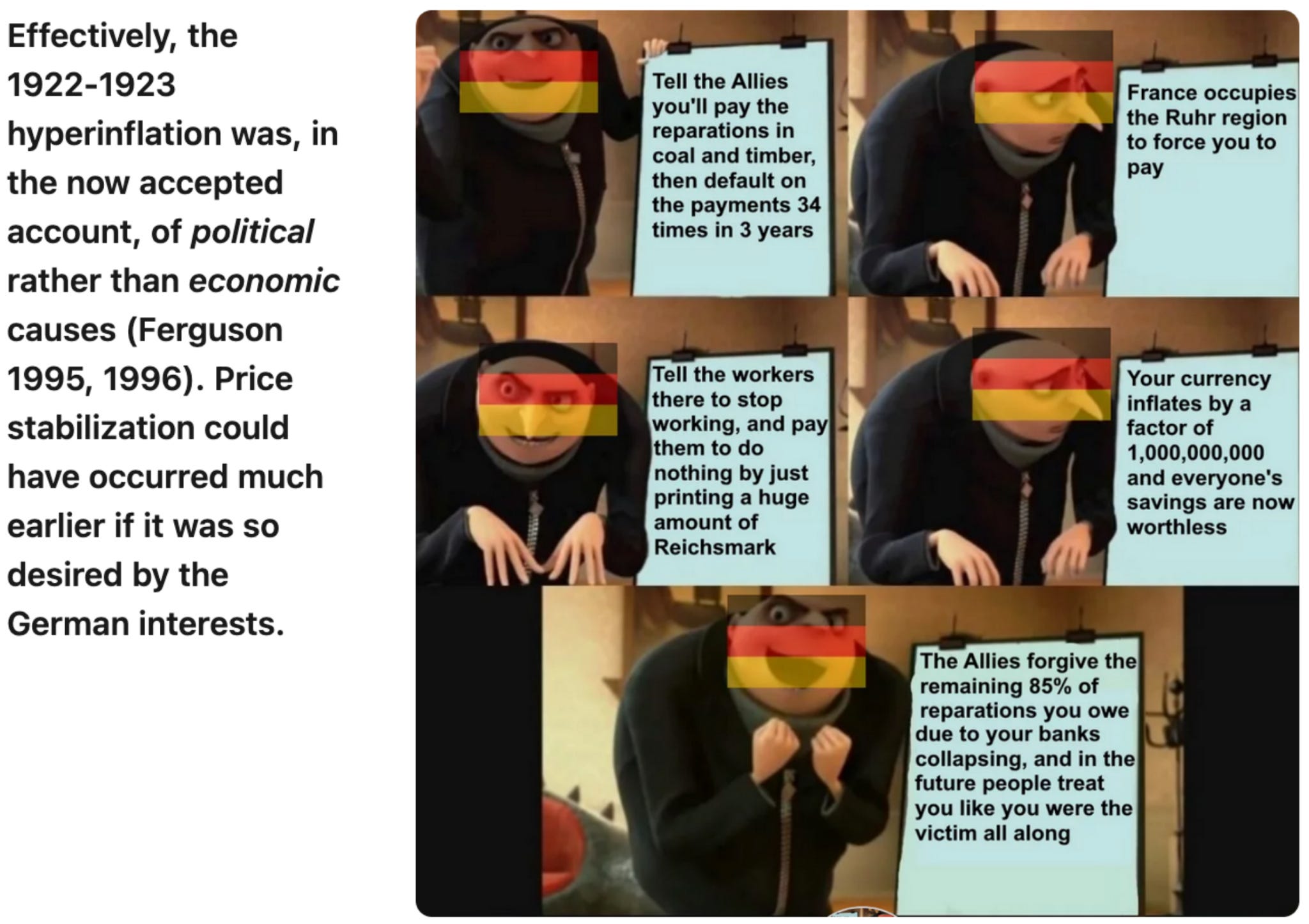

It has always and everywhere been caused by unprecedented economic collapse. Think of the Yugoslavia war and trade embargo which led to a severe exchange rate devaluation, or how Weimar Germany sabotaged its own economy, mostly on purpose, to avoid WW1 reparations, combined with near unlimited money printing (and again with a severe currency devaluation).

By the way, the Weimar Republic’s economy-crushing hyperinflation “worked”. Germany got pretty much all of its future reparations cancelled. And by the mid 1930s, Germany was a powerhouse again.

What these hyperinflationary episodes share is total fiscal-institutional breakdown. The mechanism is different, the scale is different, the preconditions are entirely different. The United States, whatever its current fiscal pathologies, has not lost its ability to collect taxes. The “rate cuts → hyperinflation” crowd are either confused about the causation or performing for an audience that isn’t checking.

The Turkey problem

The closest real-world analogue people reach for is Turkey, and it’s worth taking seriously rather than dismissing. Two strongmen. Both want(ed) rate cuts. With very different political and economic contexts.

From late 2021 into early 2023, Erdoğan pressured the Central Bank of the Republic of Turkey to cut its policy rate from 19% to 8.5%, firing three central bank governors along the way. Turkish CPI hit 85% at peak. The lira lost roughly 80% of its value against the dollar over that period.

So maybe the US would follow the same path? No.

First, Turkey was cutting rates into already-rising inflation. Near 20% before the cuts began, partly from global commodity prices and COVID supply chains. The rate cuts poured fuel on a fire that was already burning.

Second, the primary transmission mechanism wasn’t the rate cut. It was the currency collapse. Turkey runs a structural current account deficit and imports energy, food, and most intermediate goods. When the lira fell, import prices surged immediately. The exchange rate pass-through did the damage, not the policy rate itself.

Third, Erdoğan wasn’t just cutting rates. He was simultaneously running fiscal expansion and directing state banks to lend aggressively. The rate cut was one instrument in a package of policies that together destroyed the purchasing power of the lira. You can’t surgically separate it from the rest and declare causation.

Even then, Turkey did not produce hyperinflation in the Cagan sense. Not even close. If Erdoğan’s experiment is your best case for the Yellen thesis, the Yellen thesis has a problem.

So are rate cuts OK? Maybe

Here is the thing Yellen knows but hasn’t said clearly, and which matters more than the hyperinflation rhetoric.

The Fed controls the short end of the yield curve. Markets (mostly) control the long end. And it’s the long end that determines mortgage rates, corporate borrowing costs, and ultimately the total real cost of US government debt. A Fed chair who cuts short rates under political pressure doesn’t automatically cut the borrowing costs the White House actually cares about.

In fact, the opposite is likely. Every time Erdoğan pressured the CBRT to cut, Turkish long rates went higher, not lower. The market’s risk premium for political interference exceeded the rate cut itself. The policy was self-defeating. Faced with 85% inflation, Erdoğan was eventually forced into a humiliating about-face: hiking rates from 8.5% all the way back to 50%, the exact opposite of what he set out to do.

The same logic applies to the US, with higher stakes. Rate cuts might not actually accomplish what Trump might want to have happen. In fact, it could make things much worse, even without any hyperinflation.

On the other hand, as I pointed out a few weeks ago, maybe Warsh’s rate cuts will increase the demand for Treasuries. At a cost of requiring micromanagement of bond volatility. Maybe the hedgies will save the day. For a while. And rate cuts may not transmit inflation into the economy, in any event.

The opposite of hyperinflation is the worry

There is a major problem with any focus on hyperinflation. It happened in the 1930s. And lead directly to the rise of Hitler and, likely, the Second World War. Because the German government was so worried about a recurrence of the Weimar hyperinflation of 1923, they were extremely reluctant to stimulate an economy in deep depression in the early 1930s.

Deflation, a much bigger risk than hyperinflation, was the result. And political instability ensued.

I worry that Warsh and Bessent together will not do what it takes to fix a crisis. Fault Bernanke for many things, but without him, fiscal conservative Obama would never have taken the fiscal and monetary steps needed to fix the global economy in 2008 and beyond. Bessent would certainly not have the same influence, nor would he want to, being a true gold standard acolyte. Warsh might be similar. A cabinet and a Fed unwilling to do what it takes to avoid depression and deflation is the biggest risk to the global economy.

Baba Yaga is real. It's just that in 2026, she lives in the deflationary basement, not the hyperinflationary attic. And nobody seems to be checking the basement. That’s what should worry everyone.

For sure, the Warsh/Bessent years will be interesting.